Q & A with the Social Security Administration—Common Questions About Benefits and Programs

![]()

Learn about your retirement benefits as we answer some basic questions that seem to frequently come up during our educational presentations. Social Security is part of the retirement plan of almost every American worker. If you’re among the 96 percent of workers covered under Social Security, you should know how the system works.

When should you start your Social Security Retirement Benefits?

At Social Security, we’re often asked, “What’s the best age to start receiving retirement benefits?” The answer is that there’s no one “best age” for everyone and, ultimately, it’s your choice. The most important thing is to make an informed decision.

Your decision is a personal one. Would it be better for you to start getting benefits early with a smaller monthly amount for more years, or wait for a larger monthly payment over a shorter timeframe? The answer is personal and depends on several factors, such as your current cash needs, your current health, and family longevity. Also, consider if you plan to work in retirement and if you have other sources of retirement income. You must also study your future financial needs and obligations. This decision affects the monthly benefit you will receive for the rest of your life, and may affect benefit protection for your survivors.

When can I start my benefits?

You can start your Social Security retirement benefits as early as age 62, but the benefit amount you receive will be less than your full retirement benefit amount. Your monthly retirement benefit will be higher if you delay starting it. To find your full retirement age click here.

We calculate your basic Social Security benefit—the amount you would receive at your full retirement age—based on your lifetime earnings. However, the actual amount you receive each month depends on when you start receiving benefits. You can start your retirement benefit at any point from age 62 up until age 70, and your benefit will be higher the longer you delay starting it.

If I start my benefits early, how much of a reduction will I take?

If you start your benefits early, they will be reduced based on the number of months (a little more than one-half of one percent per month) you receive benefits before you reach your full retirement age. You could take a 25 to 30 percent reduction if you start early.

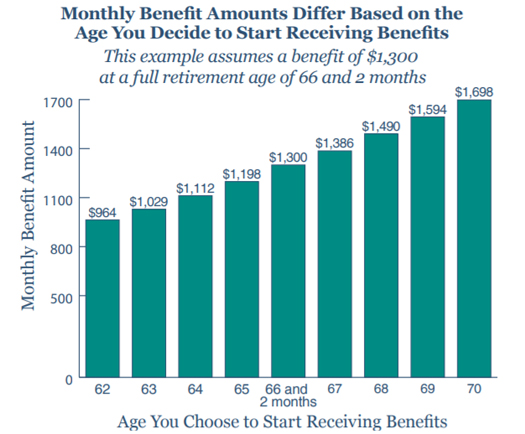

The following chart shows an example of how your monthly benefit increases if you delay when you start receiving benefits.

Let’s say you turn 62 in 2017, your full retirement age is 66 and 2 months, and your monthly benefit starting at that age is $1,300. If you start getting benefits at age 62, we’ll reduce your monthly benefit 25.8 percent to $964 to account for the longer time you receive benefits. This decrease is usually permanent.

If I wait to take my benefits after my full retirement age, will they be larger?

Yes, your benefits keep growing until age 70. If you choose to delay getting benefits after your full retirement age, you would increase your monthly benefit at the rate of two-thirds of one percent per month or eight percent per year. In our example case, your benefits would grow to $1,698. This increase is the result of delayed retirement credits you earn for your decision to postpone receiving benefits past your full retirement age. The benefit at age 70 in this example is 76 percent more than the benefit you would receive each month if you start getting benefits at age 62 — a difference of $734 each month.

Can I work after I start my Social Security retirement payments?

You can get Social Security retirement benefits and work at the same time. However, if you are younger than full retirement age and make more than the yearly earnings limit, we will reduce your benefit. Starting with the month you reach full retirement age, we will not reduce your benefits no matter how much you earn.

- We use the following earnings limits to reduce your benefits: If you are under full retirement age for the entire year, we deduct $1 from your benefit payments for every $2 you earn above the annual limit. For 2017 that limit is $16,920.

- In the year you reach full retirement age, we deduct $1 in benefits for every $3 you earn above a different limit, but we only count earnings before the month you reach your full retirement age. If you will reach full retirement age in 2017, the limit on your earnings for the months before full retirement age is $44,880.

- Starting with the month you reach full retirement age, you can get your benefits with no limit on your earnings.

For additional information about retirement benefits visit www.ssa.gov.

Contributor Kirk Larson is a public affairs specialist with Social Security Washington.